Get the latest direct to your inbox twice a week. Sign up today.

ASA annual ad spend report: TV’s lead narrows, interactive overtakes newspapers, and industry calls for greater transparency around categorisation

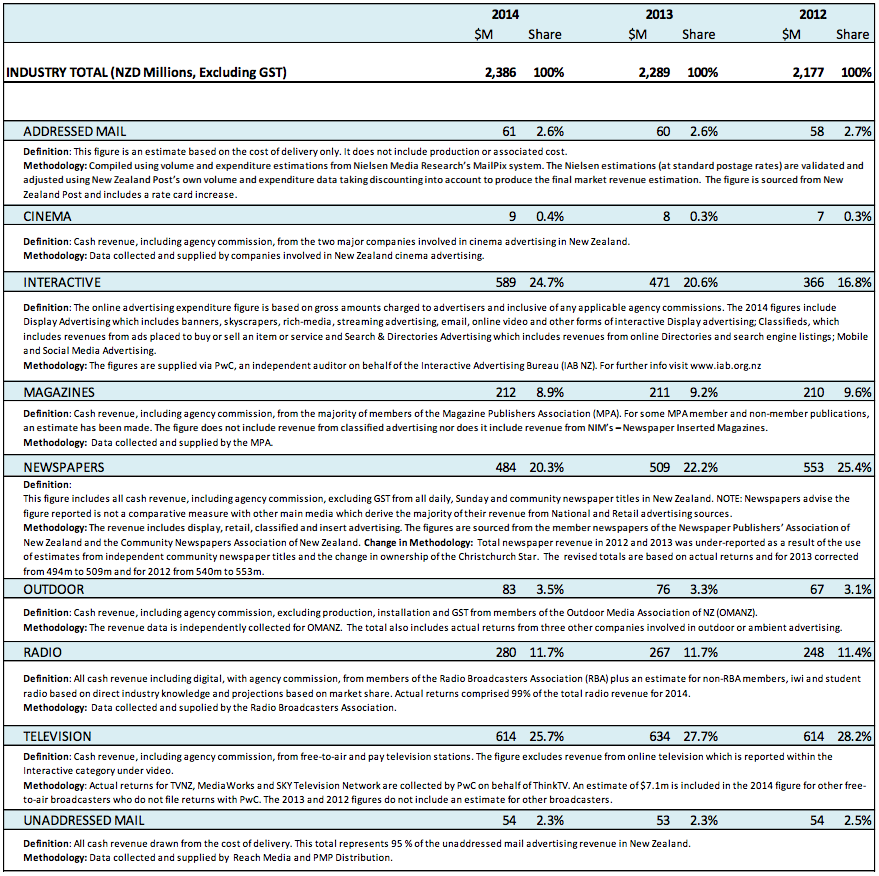

The overall ad spend pie grew by 4.2 percent to $2.39 billion in 2014, according to the Advertising Standards Authority’s figures for the 12 months ended December 31. And once again it was interactive leading the charge, overtaking newspapers and getting close to TV in the sector rankings.

In 2013, total spend was $2.29 billion and in 2012 it was $2.18 billion. So, overall, 2014 looks like a fairly positive year, with small rises in spend for all sectors aside from newspapers and TV, which both had big drops.

In terms of size, TV is still on top, but only just. Its market share decreased by two percent after a drop of $20 million to a total of $614 million. That followed last year’s increase of $20 million. But this figure excludes ad revenue from online video, which clocked in at $23 million across TVNZ, MediaWorks and Sky.

“At a topline level we’re still running revenue around 2008 levels, before recession, before any of us we had any meaningful online presence,” says Jeremy O’Brien, TVNZ’s head of sales and marketing. “So we think it’s holding its own really well.”

O’Brien says total advertising expenditure on TV shows across both on-air and online with the three broadcasters actually adds up to $637 million for 2014, which is 26.7 percent of the total advertising market. And because it feels the existing figures give an inaccurate reflection of the TV market, the networks will include VOD ad revenue in TV rather than in the interactive sector from next year.

“TVNZ, MediaWorks and Sky will provide both on-air and online revenues to the ASA,” he says. “We’re urging the IAB to also break interactive down to its four component parts of search and directories, classifieds, display, and mobile. By doing so we believe it will give advertisers more meaningful insights into the way in which marketing budgets are invested in New Zealand media.”

In its report released in February, the IAB did break its data down into these categories, providing a clearer indication of where ad spend was going but this is not reflected in the ASA data, despite the information coming from the same source (PwC’s numbers). While there was growth overall, the majority driven by search and directories, it was significant that the display advertising category dipped year on year. This trend is most likely driven by the growing sentiment among advertisers that display advertising, particularly in the form of banner ads, is ineffective.

O’Brien says interactive isn’t a sector, it’s a catch-all phrase. And the lack of detail lends itself to the uneducated making ill-informed decisions.

“It’s about giving greater visibility to help advertisers make better informed decisions … At the moment you read a sensationalist headline and you could be forgiven for thinking there’s no point putting any dollars into TV advertising. We know that is fundamentally not true.”

When asked if the decline in ad spend on linear TV is due to declining ratings, a trend being seen around the world as other viewing options like SVOD become more popular, O’Brien points to a recently released multi-screen report from Nielsen that showed 3.54m New Zealanders watched TV on a traditional TV set every week and 930,000 watched TV online. 160,000 of those are watching exclusively online. He says total time spent viewing is up from a total of 20.5 hours to 22 hours.

“This market is pretty unique. You can buy across three networks, you can reach 87 percent of the population, and you can’t do that anywhere else in the world. You could halve the amount of audience that TV reaches and it would still be one of the most cost-effective ways to reach an audience in this country. So in some ways there’s a massive long way to go before it gets concerning for advertisers. Yes, there will be fragmentation and we have to counter that. And between us all we have some different strategies to reach and monetise audiences.”

As businesses and technologies evolve, there will always be issues with categorisation. And at a time when packages are being sold across different media, or when media companies are adding revenue through production, it gets even more complicated to split it up.

Interactive added $118 million to its total, up from $471 million in 2013 to $589 million this year. This has increased its market share from 20.6 to 24.7 percent.

Newspapers are next on the list, but they have suffered the most, losing $25 million to move down the list to third on $484 million. On the plus side, the decline is smaller than previous years. This is in part because some historical changes have been made to the figures and newspapers’ contribution in 2013’s total has been raised by $15 million (it was up by $13 million in 2012). This is due to estimates being used for community newspapers and a change in ownership at the Christchurch Star.

Like TV, a small but growing proportion of its revenue comes from online sources.

Radio charted an increase of $13 million and its market share stood firm on 11.7 percent. Last year, radio was accused of inflating the numbers by adding online spend into the radio category. This year, the notes say digital spend is included in the radio category.

The next biggest category was magazines and money spent in that medium was up $1 million to $212 million. Market share is down slightly, continuing trends from previous years.

Outdoor had a good year, up from $76 million in 2013 to $83 million last year. That brings it back to the peak experienced during the Rugby World Cup in 2011.

OMANZ says the 9.2 percent year on year growth has been generated by a wide selection of advertisers across numerous categories.

“According to Nielsen data the picture across the top 20 advertisers shows an aggregated 27 percent increase in revenue over 2013. The most notable increases in outdoor spend for 2014 have come from advertisers within the telco industry, council and government agencies, grocery, breweries and media.”

With an increase in share to 3.5 percent and declines at the top of the table, it is confident it can reach its objective of achieving a total market share of five percent.

Addressed and unaddressed mail were both up by $1 million to $61 million and $54 million respectively. And cinema, the smallest chunk of ad revenue, was also up by $1 million, finishing up with $9 million.

UPDATE: ASA chief executive Hilary Souter was asked whether the ASA would consider introducing categorisation to the interactive category, but she says that this would largely depend on the members. She explains that the numbers are reported in accordance to guidelines set by the members and that any changes to the reporting would depend on them.

Souter went on to point out that the report this year included a section on the methodology used in each category in an effort to drive greater transparency.