New Zealand’s economy is in recovery, yet marketers are still working hard to win their share of consumer spend, with major retail and travel advertisers rising up to the challenge.

During the September to December quarter, consumers were shopping more intentionally in a highly promotional retail environment. Brands were forced to rethink media investment, channel mix and creative execution.

Are consumers spending more?

Yes, and no. The 2025 holiday retail period was defined by aggressive promotional activity and strategic trade-offs. Consumers bought more items, but at lower price points, showing households remained cautious and value-driven, stretching budgets even as CPI inflation eased[4]. Increased travellers to New Zealand also helped cushion softer spending[2].

The Warehouse Group reported a 2.4% decline in average selling prices, reflecting discounting and inventory pressures[3].

Retail electronic card transactions rose 1.2% in November, with apparel up 3.4%, durables up 2.1% and hospitality up 1.3%[5]. Encouragingly, spending on apparel and hospitality highlighted the value of social moments and seasonal refreshes, though more selectively.

How are retailers competing for attention?

The holiday quarter saw retail brands deploy a mix of long-running brand campaigns, tactical sale promotions and digital-first creative strategies.

The Warehouse Group leaned heavily into its established “You’ll find it at The Warehouse” video campaign, moving toward more personality, humour and engaging content on social channels[3].

Retailers leaned on strong identity and creativity to reduce reliance on discounting and support longer-term goals.

Glassons maintained a lifestyle-led social presence through user-generated content and behind-the-scenes posts, suggesting confidence in branding over promotions.

In men’s apparel, Hallenstein took an aggressive promotional stance, running Singles Day campaigns and a 20% off sale extending through major holidays. Its Smartflex campaign leveraged OOH and local sports partnerships, blending lifestyle positioning with tactical discounting.

Briscoe-owned Rebel Sport NZ‘s “It all starts here” campaign, emphasised “team sport”, creating emotional justification for full price items.

Large retailers played an early game, while smaller competitors like Archies Footwear timed their “Gifts under $50” campaign for Christmas shopping in December.

What’s happening in the travel sector?

While retail advertisers competed on brand and value, travel brands invested in premium positioning and experience-led messaging.

Helloworld Travel reported 27% growth in wholesale cruise sales across its ANZ brands, with strong performance in luxury and expedition categories. It also launched Viva Gold, a new premium tier[6]. Competitor Flight Centre Travel Group acquired Iglu to accelerate cruise growth[7], reinforcing the industry’s confidence in premium demand.

International operators, including Uniworld, HX Expeditions and Hurtigrute, promoted European river cruises and Arctic expeditions, while Intrepid Travel increasingly promoted long-distance rail trips in Asia and Europe[1].

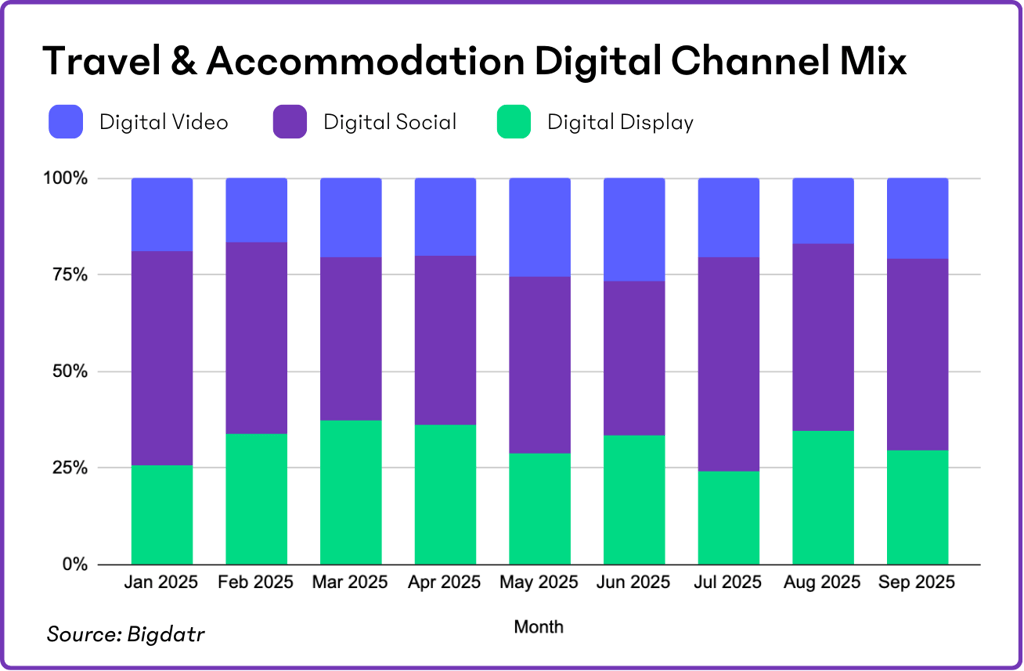

Travel media spend followed seasonal patterns: cruises peaked in February. Short-term accommodations were mostly served in January, July and August, car rentals spiked in January and June, and tours were the most competitive in September.

Social media-led digital investment peaked in January and July, while digital display peaked in March, June and August, with September attracting the highest digital spend[1].

The data also showed strong outbound travel momentum, with domestic spend down in November 2025 year on year, while international spend rose[8], signalling prioritisation of high-value experiences and increased pressure on local tourism.

How travel brands communicate the value of experiences

Domestically, travel brands aligned with Tourism New Zealand’s focus on active travel and digital disconnection. Walking, hiking and tramping were the top activities among international visitors at 62% – up from 58% in 2024, with advertisers promoting “digital detox” experiences online[9].

Targeted local campaigns included New Zealand’s Guide’s South Island stays, Flight Centre and Contiki’s Rhythm and Alps packages and Franz Josef Glacier Guides year-long premium glacier campaign – all driven by emotional experiences rather than competing on price.

Quick recap and what’s ahead for 2026 advertising

- Track retail promotional calendars: With brands like Hallenstein running overlapping sales from Singles Day through to Boxing Day, understanding competitors’ timing and promotional benchmarks is critical to protecting margin and share. Daily creative and activity tracking is available with Bigdat’s Advertising Creative.

- Monitor creative strategies and channel mix: Glassons has a unique presence across Australia and New Zealand, as shown in one of the 75+ industries tracked by Bigdatr. Social media dominated in New Zealand over summer and winter, while Australia had a stronger social media allocation in April, May and September.

- Map your competitive set broadly: Local brands aren’t just competing with each other, but also with international competitors like Uniworld and Hurtigruten. Intrepid Travel led the growing rail travel segment. Tracking brands across your market helps you understand what local consumers see in digital and offline spaces.

- Benchmark media investments: By understanding local competitors like Tourism New Zealand’s “digital detox” experiences online, you can see where competitors are investing and the share of voice they capture. Travel category data also showed tours, short-term accommodation, cruises and car rentals leading media value, each with distinct peaks, revealing seasonal trends to guide successful planning.

For marketers looking to understand competitors, Bigdatr keeps you connected to the advertising landscape by monitoring major advertisers and media channels every day. Learn more at bigdatr.com