Get the latest direct to your inbox twice a week. Sign up today.

Nielsen’s Caroline Atford on responding to fragmentation

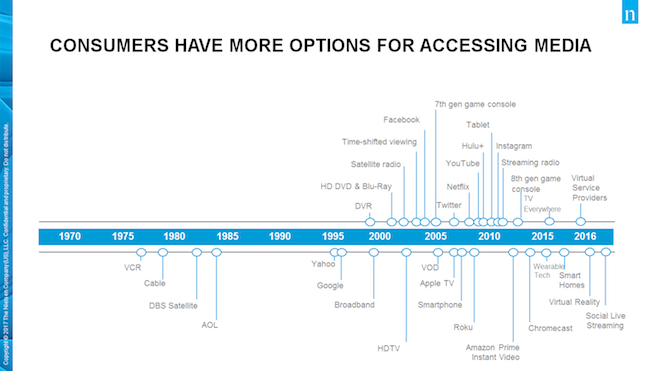

Can you believe it’s eight years since the launch of the iPad? Would you have predicted in 2009 that the following year would see a tablet change the world?

Sitting down to speak to Caroline Atford, executive director of media in Nielsen New Zealand, she says fragmentation is the biggest change to the industry as a result of advancement in technology and increased mobility in the past 10 years.

After 16 years with Nielsen working with agencies and clients, she’s seen the rise of digital technology create a traditional versus digital view, with many having two different strategies and two different budgets.

But, when flipping the picture and putting the consumer first, it’s a view that needs to stop because audiences do not see the digital and traditional comparatively.

“If you ask the average consumer now, I would say most of them are more focused on the content and they don’t really care how they are accessing it,” Atford says.

“Whether they have picked up a newspaper and read an article through to seeing it online, hearing it on the radio or seeing it on the TV, all they know is they have heard the content they needed to catch up on.”

And as well as audience fragmentation, Atford sees changes in the readiness of consumers to embrace new technology, with older generations far more receptive than they once were.

Looking back, she says it’s always been the case that older and younger audiences would consume media differently as the younger generation would morph into the older and pick up the habits of the previous generation.

Now, she sees the older generation learning the ways of the digital world by picking up on what younger people are doing and running with it.

“They are open to being taught, they want to see what the younger people are involved in and it’s there’s not such a divide.”

Measuring up to the change

But how have these changes impacted audience numbers? Has fragmentation fragmented ratings and made audiences hard to find?

The answer is yes and Atford says Nielsen is working to make sure its measurement abilities are responding to the changes.

Early last year, the company announced its Digital Ad Ratings service in New Zealand that measures the demographics, unique audience, reach, frequency and gross rating points (GRPs) for an ad campaign’s full digital audience across computers, tablets and smartphones.

It has been trialled in the local market prior to its rollout and had proven success in the US where it had been in play since 2011.

Atford describes it as “a good read of what’s happening in the advertising space” as it provides agencies and clients with a true understanding of the reach and the frequency measure for their ad campaign.

At the time, Nielsen New Zealand director Tony Boyte told StopPress it was the first measurement service of its kind, and investment to bring it to the local market is a reflection of digital’s rapid growth as an advertising platform.

“Digital has been around for a number of years, and it’s been easy for pumping out the volumes of impressions and trying to reach what we think is mass reach, but advertisers are now looking at that and going: ‘Well, I need to start measuring my return on investment. It’s no longer the early days of digital advertising where it’s something we just do; we have to see if it is giving bang for buck.’”

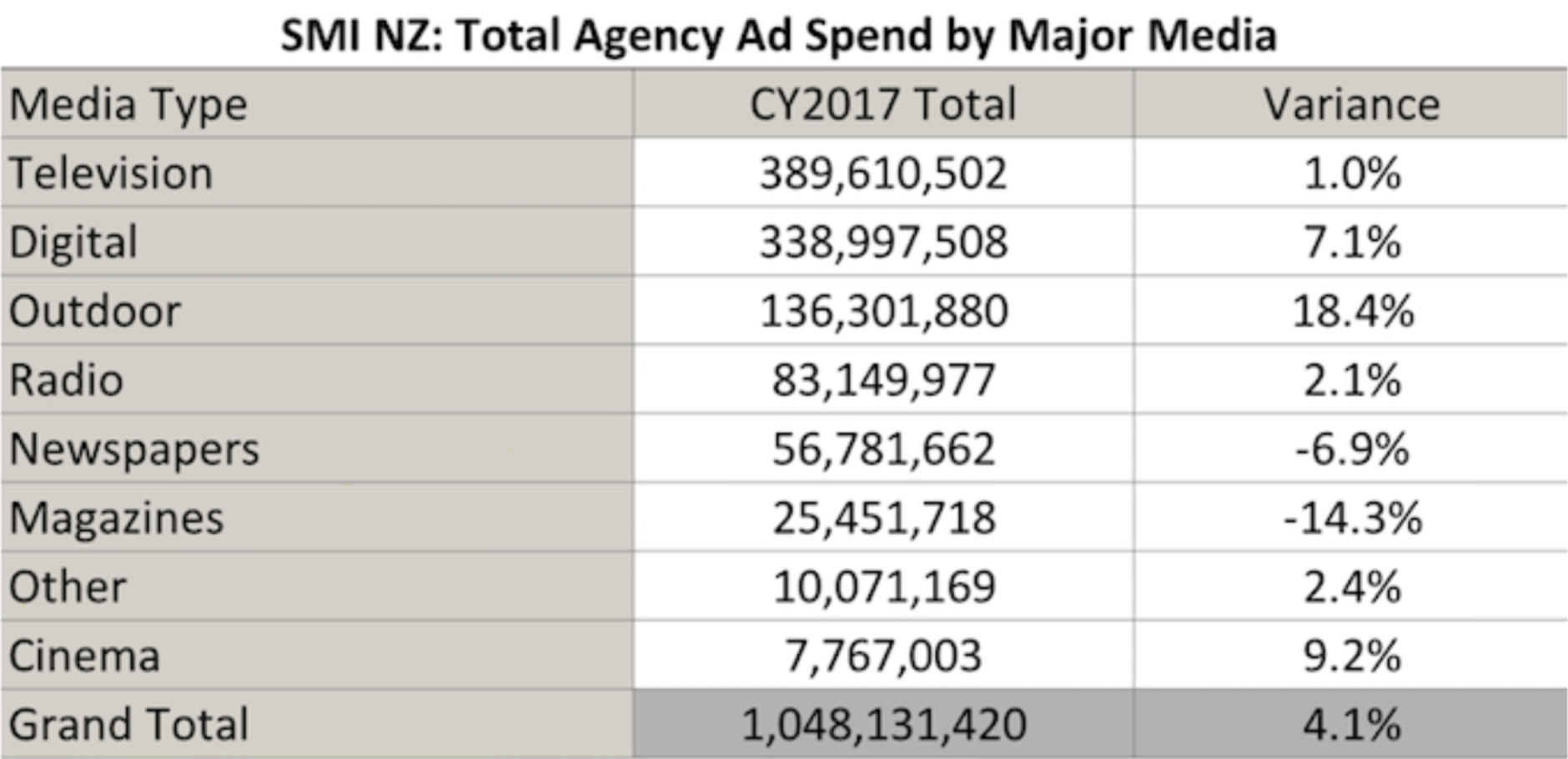

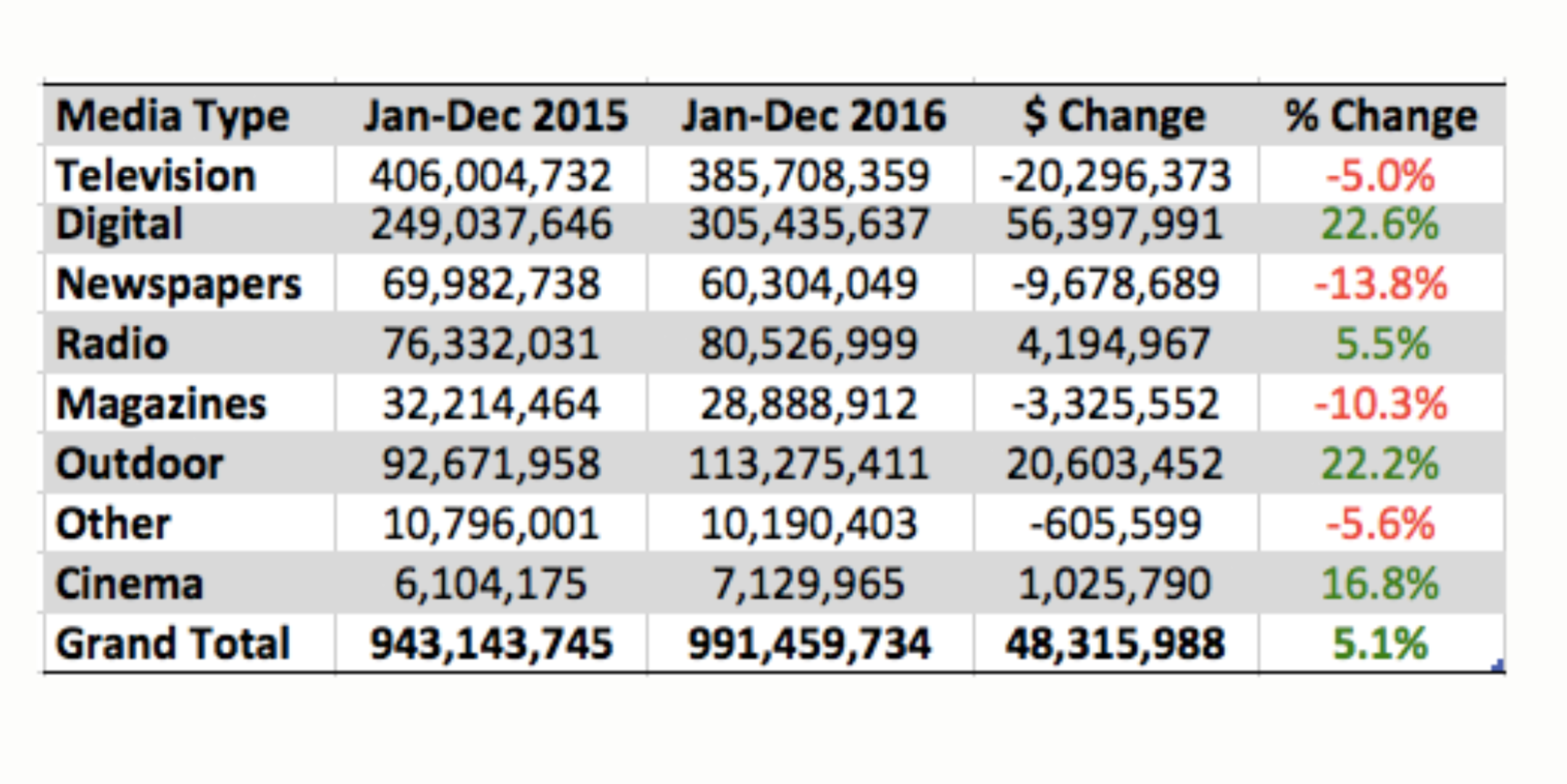

Clients taking a considered approach to digital advertising is reflected in the Standard Media Index’s (SMI) total agency ad spend by major media for 2017.

While television continues to see the greatest income, digital’s rise is slowing. Between 2015 and 2016, it grew 22.6 percent, whereas between 2016 and 2017, it grew 7.1 percent.

In the same period, TV saw a five percent drop before a one percent increase.

Looking beyond digital ad measures, Atford says Nielsen’s next step will be to look at providing a robust measure of content. She says the improvements are being made with Nielsen’s Digital Content Ratings, in the US and Australia, measuring all content types including video and text with metrics fully comparable to TV.

And now it’s time to put them into the local market and get the industry used to working with them.

“We’re excited we have the Digital Ad Ratings out there and we are working very closely with the industry to roll out the next stage – digital content ratings, so to have those two pieces to the puzzle is a great step forward for us.”

Busting myths

While SMI’s numbers show TV is still the strongest channel from an advertisers perspective, the questions of its strength in the face of digital’s rise is one lingering in the background of the industry.

However, Atford points out that while new technologies have offered alternative screens to the TV, new technologies, such as smart TVs, Apple TV and Chromecast, are giving TVs a new lease on life.

“All those things have completely changed the way people engage with their TV,” she says, with no mention of audiences stopping their engagement with the TV altogether.

“The TV set is still clearly the dominant screen, but the way people are watching it is definitely changing.”

And letting the numbers speak alone, there’s no arguing TV is the most popular screen, with New Zealanders spending more than 21.5 hours a week watching broadcast TV across a week—over six hours more than Internet users spend online per week (Nielsen Television Audience Measurement [TAM], All People 5+, Nielsen Consumer and Media Insights, Q1 – Q4 2016, All People 10+).

For those who are in agreeance with the idea that TV is dying, Atford reminds them to look beyond their own scope of content consumption.

“The challenge we all face is we think our lives represent everyone’s lives but that’s not the case. It’s easy to have an opinion versus what you do yourself but it’s important to look at the data and remind yourself what’s happening in the wider population.”

This point was proven in a News Works survey, run on StopPress last year, that tested the knowledge of 510 would-be media gurus across the New Zealand marcomms industry. Not one participant got a perfect score.

New Zealand’s shrinking distance

While the fact the Digital Ad Ratings ability and Nielsen’s Digital Content Ratings measures have been available in markets prior to being introduced locally may seem like an example of New Zealand being behind the rest of the world, Atford says the county is one of Nielsen’s lead markets – meaning there’s a focus from the global leadership as far as priority product roll out.

Also helping is the scalability of the new measurement systems, as those previously in place in the US have not been able to be introduced to New Zealand due to its size.

Now, Atford explains they have been developed so it doesn’t matter what size the market is and New Zealand is on a journey closer to that of the US and Australia than we’ve ever been before.

“What I think’s going to happen is the lag we’ve seen happen historically between what happens overseas and what happens in New Zealand is going to get closer and closer and disappear,” she says.

“Technology gets rolled out now and it arrives in New Zealand just as quickly as it arrives everywhere else. It’s not like the old days we had to wait three years for it to arrive on a boat.”

That shrinking gap is one of the aspects she considers to be exciting when looking into the future in the years ahead and while she cannot predict what’s to come, she looks forward to seeing it.

“If we sat before the year before the iPad came out, I don’t think anyone would have gone: ‘Wow, there’s going to be a little tablet that changes the world.’ Nobody would have predicted that.”